Manchester Property Market Forecast 2026

Prices, Yields, Area Analysis and the 5-Year Outlook

The Complete Guide for Buyers, Landlords and Overseas Investors

Average price 254,000. Annual growth 4.4%. JLL: 19.3% five-year growth. Savills: 28.8% North West by 2028. The full 2026 Manchester forecast explained in plain English.

Manchester Property Market, Headline Statistics 2026

254k Avg price Jan 2026 (ONS) | +4.4% Annual price growth (YoY Jan 2026) | 28.8% 5-yr NW forecast (Savills, to 2028) | 19.3% Manchester 5-yr forecast (JLL, to 2028) |

IN THIS GUIDE

- Manchester in 2026: The Starting Point

- Manchester Property Market Forecast 2026: The Numbers in Full

- The Manchester Rental Market Forecast for 2026

- Manchester Property Market Forecast 2026: Area-by-Area Analysis

- Why Supply and Demand Still Favour Manchester Buyers and Investors

- The Economic Drivers Behind the Forecast

- Manchester Property Market Forecast 2026: What It Means for Investors

- Risks to the Forecast: What Could Disrupt Manchester’s Growth?

- Frequently Asked Questions

- The 2026 Verdict and CTA

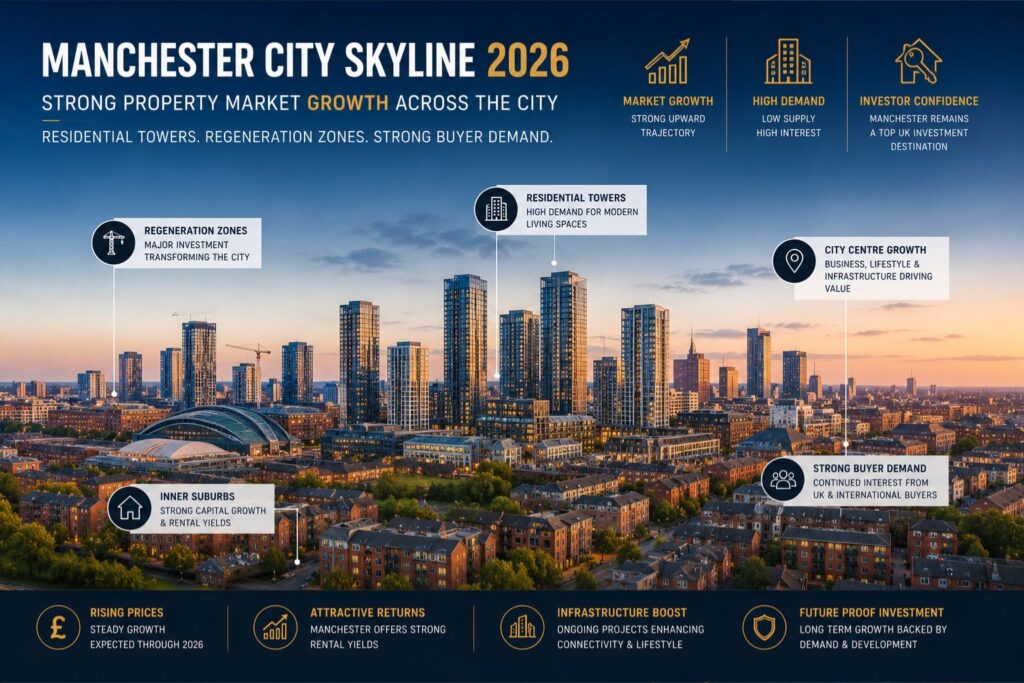

1. Manchester in 2026: The Starting Point

The Manchester property market forecast for 2026 begins from a position of genuine strength. The average property price in Manchester reached 254,000 in January 2026, a 4.4% year-on-year increase (ONS), while 18,426 property transactions were recorded between January and August 2025, confirming the city’s status as one of the most active residential markets in England outside London. Rents averaged 1,330 to 1,345 per month across the city, with gross yields ranging from 6% to 6.6% on standard residential stock and up to 9% in HMO hotspots such as M14 Fallowfield.

What makes 2026 particularly significant is the alignment of conditions that have rarely converged simultaneously: the Bank of England’s December 2025 rate cut to 3.75% has unlocked pent-up buyer demand; a structural undersupply of housing continues to support both prices and rents; and Manchester’s corporate economy, home to Amazon, Google’s only UK office outside London, ITV’s joint headquarters, and AstraZeneca, is delivering employment growth at 1.8% annually, the highest of any major UK city. This is the backdrop against which every forecast figure in this guide should be read.

For investors, this context is not academic. It is the fundamental reason why Manchester has outperformed the UK average on both price growth and rental income for the past decade, and why the mainstream forecasters, JLL, Savills, Investropa, all project it to continue doing so through 2028 and beyond.

“Manchester’s housing market in 2026 is forecast to offer stable, sustainable growth with reliable rental upside. Property prices are projected to grow by 4.0% to 5.5%, supported by continued undersupply, improving mortgage affordability, and strong inward migration.”

, The Luxury Playbook, Manchester Real Estate Market Forecast, 2026

2. Manchester Property Market Forecast 2026: The Numbers in Full

The table below consolidates the most widely cited and credible forecasts for Manchester property prices and rents across both the short-term 2026 view and the medium-term outlook to 2028 and 2030.

Manchester Property Price and Rental Forecasts, 2026 to 2028, Consolidated Forecaster Data

Forecaster | 2026 Price Growth | 5-Year Cumulative | Notes |

JLL | 4.0% | 19.3% to 2028 | Manchester ranked 2nd strongest UK city for price growth to 2028 |

Savills (North West) | 5.5% | 28.8% to 2028 | Year-by-year: 4.5% in 2025, 5.5% in 2026, 6.5% in 2027, 5.5% in 2028 |

Investropa | 3% to 5% | 25% to 30% to 2030 | Base case; optimistic scenario 35% if rates fall faster than expected |

TK Property Group | 3% to 4% | 15% to 20% to 2029 | Conservative estimate; local supply and demand dynamics central to projection |

The Luxury Playbook | 4% to 5.5% | Positive | Emerging districts 4.5 to 5.5%; mature zones 3 to 4.5% annually |

Rothmore Property | 3% to 4% | Broadly positive | Gross yields 6 to 6.6%; demand outpacing supply in all scenarios |

JLL Rental Forecast | 4% per year | 21.7% to 2028 | Only Birmingham and Edinburgh expected to outperform Manchester rental growth |

The most important observation from this consolidated table is the consistency of direction across all forecasters, even where the precise figures differ. Every credible analysis points to positive price growth in Manchester in 2026, with the range from 3% to 5.5% reflecting different assumptions about the pace of Bank of England rate reductions and the speed at which buyer demand translates into completed transactions. For investors, this unanimity of direction matters more than the width of the range.

The five-year view is where the real opportunity becomes clear. Savills’s 28.8% North West projection, JLL’s 19.3% Manchester-specific figure, and Investropa’s 25% to 30% base case all point to a market that will deliver materially above-average capital appreciation through to 2028 or 2030. The UK national average growth forecast over the same period is 17.6% (JLL), meaning Manchester buyers are positioned to outperform the national market by 2 to 11 percentage points on capital growth alone, before rental income is considered.

“As of early 2026, the estimated cumulative property price growth expected over the next five years in Manchester is approximately 25% to 30%, based on mainstream forecaster projections. The average annual appreciation rate is approximately 4.5% to 5.5% per year, outpacing the UK national average and most southern regions outside London.”

3. The Manchester Rental Market Forecast for 2026

The rental component of the Manchester property market forecast 2026 is, for many investors, the more immediately relevant figure. Capital growth is realised over years. Rental income arrives every month. The outlook for both is positive, but the rental picture is particularly strong.

JLL forecasts annual Manchester rental growth of 4% per year through to 2028, placing the city second only to Birmingham and Edinburgh among major UK cities. Cumulatively, this represents 21.7% rental value growth from 2024 to 2028, a figure that significantly outpaces projected price growth in most comparable UK cities and underscores the structural strength of Manchester’s rental market. Monthly rents averaged 1,330 to 1,345 in early 2026, with prime city centre one-bedroom apartments in Ancoats and the Northern Quarter commanding 1,300 to 1,600 per month.

The driver of this rental strength is straightforward: there are simply not enough homes to rent. Nationally, there are 25.4% fewer properties available to rent than a decade ago, and Manchester’s undersupply is among the most acute in the UK. The city’s 100,000-plus student population, generating 36,000 graduates annually with a 51% local retention rate, creates perpetual demand from a well-qualified tenant base that can absorb rental increases without significant void pressure.

The HMO segment is the highest-performing rental sub-market. Fallowfield’s M14 postcode consistently achieves gross yields of up to 9%. Clayton, Gorton, and Salford are all delivering yields of 6.5% or above according to PropertyData. The Renters Rights Act, which came into force on 1 May 2026 and abolished Section 21 no-fault evictions, has deterred some less committed landlords from the market, further tightening supply and supporting rental prices for professional operators who remain.

“JLL forecasts robust rental gains for Manchester, predicting annual increases of 4.5% in 2025, 4% in 2026, 3.5% in 2027, and 3% in 2028. This results in cumulative rental growth of 21.7% over the period, with only Birmingham expected to outperform Manchester.”

Miller Rose, Manchester House Price Predictions, November 2025

4. Manchester Property Market Forecast 2026: Area-by-Area Analysis

Manchester is not a monolithic market. The 2026 forecast varies significantly by postcode, property type, and proximity to regeneration activity. The area-by-area breakdown below draws on The Luxury Playbook’s 2026 analysis, which identifies distinct growth corridors within the wider city.

Emerging Regeneration Districts: Hulme, Ardwick, Newton Heath and Victoria North

The strongest price growth in 2026 is forecast for Manchester’s emerging regeneration zones, which are expected to achieve 4.5% to 5.5% annually. The Victoria North masterplan, a 15-year, 14,000-home programme covering Red Bank and Collyhurst, is the most significant of these, with early-phase buyers positioned to benefit from both rising land values and infrastructure improvements that will appreciably change the character of the area over the next decade. Hulme and Ardwick are attracting buyer interest as spillover from the established Ancoats and Castlefield markets pushes buyers into adjacent postcodes where value is still accessible.

Established City Centre Zones: Ancoats, Salford Quays and Castlefield

Ancoats, Salford Quays, and Castlefield are the mature segments of Manchester’s city-centre market. Growth here is projected at 3% to 4.5% annually, below the emerging zone forecast but underpinned by the deepest tenant demand and the strongest letting velocity. Ancoats one-bedroom apartments are letting in an average of 22 days. Salford Quays benefits from the BBC and ITV employment anchor. Castlefield offers the rarest commodity in Manchester, genuine urban heritage in a city-centre setting. These zones are best suited to investors prioritising yield consistency and exit liquidity over maximum capital growth.

South Manchester Family Suburbs: Didsbury, Chorlton and Heaton Moor

Semi-detached and detached houses in South Manchester’s family suburbs are consistently the strongest performers on capital growth, with annual appreciation of 5% to 6.2% on semi-detached stock (ONS data, 2026). Didsbury, Chorlton, Heaton Moor, and Sale benefit from a combination of excellent school catchments, village-scale high streets, and a persistent supply shortage in family housing. These markets are dominated by owner-occupiers rather than investors, which is precisely why they have outperformed investor-heavy city-centre postcodesacross multiple economic cycles.

High-Yield Inner Suburbs: Fallowfield, Clayton, Gorton and Longsight

Fallowfield (M14) leads the city for raw yield performance, achieving up to 9% gross on HMO properties. Clayton, Gorton, and Longsight are all delivering 6.5%+ yields on standard single-let stock. These postcodes serve a mixed tenant base of students, young professionals, and established local families. Price growth is more modest than the city centre or South Manchester, but the income profile is the most compelling in the wider Manchester market for investors whose primary objective is cash flow rather than capital appreciation.

5. Why Supply and Demand Still Favour Manchester Buyers and Investors

Every credible element of the Manchester property market forecast 2026 is ultimately underpinned by one structural reality: the city needs far more homes than it is building. Manchester City Council has consistently highlighted the pressure created by population growth, and the UK Government’s target of 300,000 new homes per year nationally is being missed by a significant margin. Manchester’s pipeline, while larger than almost any other regional city, is still insufficient to meet the demand generated by its growing population, thriving universities, and expanding corporate economy.

The 1 billion Good Growth Fund, the continuing Metrolink expansion, and the Bee Network integration are all increasing the accessibility and attractiveness of Manchester’s housing, which tends to lift demand faster than it increases supply. The Victoria North masterplan will deliver 14,000 homes over 15 years, meaningful at scale, but spread over a period long enough that the near-term supply-demand imbalance is unlikely to resolve. Deloitte’s 2026 Crane Survey recorded 4,448 homes completed in the Manchester market in the preceding year, with 11,765 under construction. On an annual delivery basis, the city needs approximately 5,000 to 6,000 new homes per year to keep pace with demand growth. Actual delivery is consistently falling short.

This supply constraint is the single most important reason why Manchester property has been a reliable investment over the past decade and why the mainstream forecasters project it to continue in that role through the next five years. Demand is structural and consistent. Supply is chronically insufficient. Price and rent levels will continue to reflect that imbalance until delivery catches up with demand, and there is currently no credible projection that suggests it will do so within the five-year forecast horizon.

6. The Economic Drivers Behind the Manchester Property Forecast

Property forecasts are only as robust as the economic assumptions that underpin them. For Manchester, those assumptions are grounded in visible, measurable economic activity rather than speculative projections.

Economic Driver | How It Supports the 2026 Property Forecast |

Corporate base growth | Amazon, Google (only UK office outside London), ITV joint HQ, AstraZeneca, Heinz. New employer arrivals annually sustain professional tenant demand. |

Employment growth 1.8% per year | Highest among major UK cities. More jobs mean more people needing housing, supporting both purchase and rental demand simultaneously. |

GDP growth 2.1 to 2.5% annually | Nearly double the UK average of 1.2 to 1.4%. City economy expanding in real terms, attracting further investment and in-migration. |

Population growth 1.24% per year | Second fastest region in England. Net gain of approximately 7,000 residents per year creating structural housing demand floor. |

University pipeline | 100,000+ students, 36,000 graduates annually, 51% retention rate. Self-replenishing professional tenant base with growing income capacity. |

Infrastructure investment | 1bn Good Growth Fund, Bee Network expansion, Metrolink growth. Accessibility improvements raise property values in adjacent corridors. |

Bank of England rate at 3.75% | December 2025 cut improved mortgage affordability. Buy to let rates falling below 5%. Released pent-up buyer and investor demand. |

Regeneration pipeline | Victoria North 14,000 homes over 15 years, Northern Gateway, Stockport Interchange. Sustained long-term investment signals. |

What Would Change the Forecast? The primary risk to the Manchester 2026 property forecast is an unexpected reversal of Bank of England rate cuts, which would delay the affordability improvement that is releasing buyer demand currently sitting on the sidelines. A significant national economic shock, recession, rapid unemployment growth, would reduce in-migration and corporate investment, weakening both price growth and rental demand. Manchester’s diversified economy provides more resilience than single-industry cities, but it is not immune. An unexpected surge in housing delivery above 6,000 units per year sustained for two or more consecutive years would begin to ease the supply-demand imbalance that underpins pricing. Given the current pipeline data, this scenario is considered unlikely within the five-year forecast horizon. Regulatory changes beyond those already implemented (Renters Rights Act, SDLT increases) could further reduce landlord supply and tighten rental availability, which paradoxically supports rental prices even as it raises compliance costs. |

7. Manchester Property Market Forecast 2026: What It Means for Investors

For investors, the Manchester property market forecast for 2026 translates into a clear, actionable investment thesis: buy now, hold for five to ten years, and allow the compounding of rental income and capital growth to deliver the total return. The consolidated forecaster data points to 3% to 5.5% price growth in 2026 alone, with a five-year view of 19% to 29% depending on the scenario. At current yields of 6% to 9% gross on Manchester residential property, the income component is delivering meaningful annual returns before capital growth is even considered.

For Pakistani and Gulf diaspora investors, the GBP income dimension adds a further layer of value. Rental income in sterling provides a natural hedge against Rupee or Dirham depreciation, and the Bank of England’s 3.75% rate in 2026 represents an attractively stable monetary environment compared to many emerging market central bank rates. Around 1 in 10 overseas buyer applications now target the North of England, double the share from 2015, and Manchester accounts for the largest share of that overseas demand outside London.

INVESTOR SNAPSHOT, MANCHESTER 2026 FORECAST IN NUMBERS Current avg Manchester price: 254,000 (ONS, January 2026) 2026 price growth forecast: 3% to 5.5% depending on location and property type 1-year value gain (on 254,000): 7,620 to 13,970 on an average-priced asset 5-year cumulative growth (base): 19.3% (JLL) to 28.8% NW (Savills) 5-year value on 254,000 (base): 309,000 to 327,000 by 2028 to 2030 Average gross rental yield: 6% to 6.6% city-wide; 9% in M14 HMO hotspot JLL rental growth forecast 2026: 4% annual increase, 21.7% cumulative to 2028 Monthly rent (city centre 1-bed): 1,300 to 1,600 per month at current market rates Average letting time (new build): 25 days from market to tenancy Optimal investor strategy: Long hold (7 to 10 years), professionally managed, diversified by zone and type |

8. Risks to the Forecast: What Could Disrupt Manchester’s Growth?

A responsible market forecast must acknowledge the risks alongside the opportunities. The following factors represent the most credible potential disruptions to the Manchester 2026 property outlook.

Risk Factor | Assessment for Manchester 2026 |

Interest rate reversal | If Bank of England reverses December 2025 cut, buyer affordability improvement stalls. Most forecasters consider this unlikely given inflation trajectory. |

National economic slowdown | A UK-wide recession would dampen employment growth and in-migration. Manchester’s diversified economy offers above-average resilience versus single-industry cities. |

Oversupply in city centre flats | New build apartment delivery is high. If investor demand softens simultaneously, city centre flat prices could underperform the broader forecast. |

Renters Rights Act complications | Professional landlords are managing compliance effectively. Amateur landlords are exiting, tightening supply. Net effect on rents is broadly positive. |

EPC regulation costs | Properties below C rating require upgrade investment. This is a manageable cost for prepared landlords but an unexpected liability for those who have not planned for it. |

Political and tax risk | Further SDLT increases or landlord tax changes are possible. Always model tax implications into the return calculation, not as an afterthought. |

The balanced assessment is that Manchester’s 2026 property market outlook is genuinely positive, but not without manageable risks. The risks are concentrated in the city-centre new-build segment and in the regulatory compliance space. Investors who buy established stock in well-performing postcodes, hold over a full market cycle, and operate professionally within the regulatory framework are exposed to those risks to the minimum degree. The risk profile is most elevated for short-hold investors in investor-heavy new-build schemes where the exit pool is narrow and the margin of safety is thin.

9. Frequently Asked Questions

What is the Manchester property market forecast for 2026?

The Manchester property market forecast for 2026 shows price growth of 3% to 5.5%, depending on location and property type. JLL projects 4% growth for Manchester specifically, while Savills forecasts 5.5% for the North West region. The average Manchester property price stood at 254,000 in January 2026 (ONS), up 4.4% year on year. Rental growth is forecast at 4% per year through to 2028 (JLL), with average monthly rents of 1,330 to 1,345.

Will Manchester house prices rise in 2026?

Yes, according to all major forecasters. JLL projects 4% growth, Savills up to 5.5% for the North West, TK Property Group 3% to 4%, and Investropa 3% to 5%. The key drivers are persistent undersupply, improving mortgage affordability following the Bank of England’s December 2025 rate cut to 3.75%, strong employment growth at 1.8% annually, and continued population expansion. Emerging regeneration zones such as Victoria North and Hulme are projected to outperform the city average.

What is the five-year Manchester property price forecast?

The five-year outlook for Manchester property prices is broadly positive across all mainstream forecasters. JLL projects 19.3% cumulative growth to 2028, outpacing the UK national average of 17.6%. Savills projects 28.8% cumulative growth for the North West by 2028. Investropa’s base case is 25% to 30% cumulative growth to 2030, with an optimistic scenario of 35% if interest rates fall faster than expected. The projected average property price in Manchester by 2030 to 2036 is 309,000 to 365,000, depending on scenario.

What rental yields can investors expect in Manchester in 2026?

Gross rental yields in Manchester average 6% to 6.6% across standard residential stock, with the Fallowfield M14 postcode achieving up to 9% on HMO properties. Clayton, Gorton, and Salford are delivering 6.5%+ on single-let stock. Average monthly rents sit at 1,330 to 1,345 city-wide, with prime city-centre one-bedroom apartments achieving 1,300 to 1,600. JLL forecasts 4% annual rental growth through 2028, delivering cumulative rental income growth of 21.7% by 2028.

Is now a good time for overseas investors to buy in Manchester?

Yes, based on the 2026 data. The Bank of England rate cut to 3.75% in December 2025 has improved buy-to-let mortgage affordability, with rates falling below 5% for many borrowers. Savills projects 28.8% cumulative North West price growth to 2028. Overseas buyer interest in the North of England has doubled since 2015, with Manchester accounting for the largest share. Non-UK-resident buyers pay a 3% SDLT overseas buyer surcharge plus the 5% BTL surcharge. Pin92 provides end-to-end acquisition support for Pakistani and Gulf diaspora investors.

10. The 2026 Verdict and Investment Outlook

Manchester’s 2026 property market is not a speculation story. It is a compounding fundamentals story. Every major element of the investment case rests on observable, quantifiable trends that have been building for a decade and are projected by credible institutions to continue for another five years: population growth, employment growth, rental supply deficit, infrastructure investment, and an economic diversification that insulates the city from single-sector downturns.

The Manchester property market forecast for 2026 points unanimously to positive price growth of 3% to 5.5%, rental income growth of 4% per year, and a five-year capital appreciation of 19% to 29% depending on scenario. For investors who buy the right property in the right postcode, hold through the full cycle, and manage their assets professionally, these are not projections. They are the expected outcomes of a well-researched, well-executed investment in one of the UK’s most consistently performing regional property markets.

The risks are real but manageable: interest rate volatility, oversupply in specific city-centre flat segments, and regulatory compliance costs all require active monitoring. For investors who model net yields honestly (not gross), who select postcodes with genuine tenant demand rather than simply headline yield figures, and who plan their SDLT and tax position from the outset, the 2026 Manchester property market represents a rare combination of income reliability and capital growth potential that very few global cities can match at this price point.

Invest in Manchester’s Growth Story with Pin92 Pin92 connects Pakistani and Gulf diaspora investors with the best Manchester property opportunities, backed by 2026 forecast data, honest advice, and end-to-end acquisition support. SPEAK TO A PIN92 ADVISOR TODAY pin92.uk | info@pin92.uk | +44 7436 899600 |